Tax Avoidance vs Tax Evasion: Know the Line

There's a question I hear more than almost any other: "Am I still on the right side of the law?" The fact that clients ask it is a good sign. The fact that so many aren't sure is a problem.

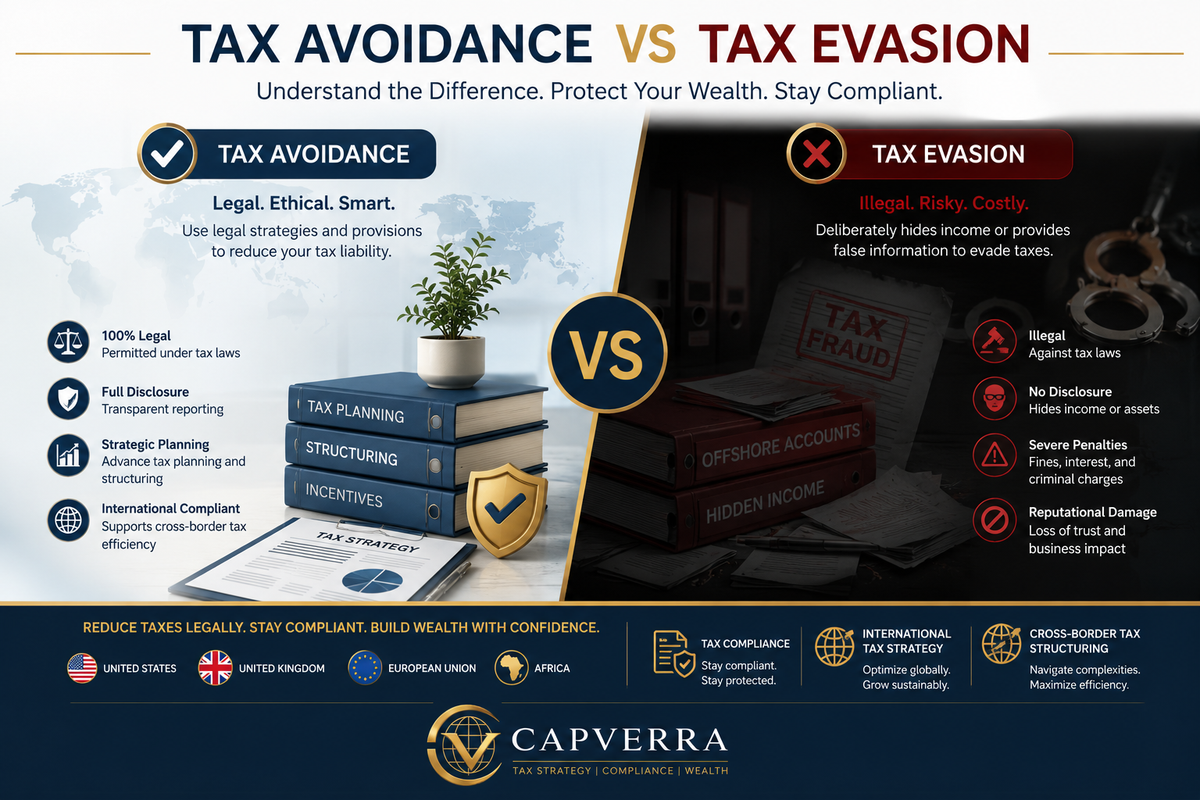

The words "tax avoidance" and "tax evasion" are used interchangeably in the media. They shouldn't be. One is a fundamental right of every taxpayer — recognised by courts in the US, UK, and most of the EU. The other is a criminal offence. Understanding which is which isn't just an academic exercise: it's the foundation of every sound international tax strategy, and getting it wrong can cost you far more than the taxes you were trying to save.

Let me explain the distinction clearly, walk you through where the real danger zones lie, and show you what genuinely effective — and legal — cross-border tax planning looks like in practice.

Tax Avoidance: Reducing Taxes Legally Is Your Right

Tax avoidance means arranging your affairs within the bounds of the law to minimise the amount of tax you owe. Full stop. The UK's House of Lords put it plainly back in 1936 in the landmark Duke of Westminster case: every person is entitled to organise their affairs so that the tax attaching to them is less than it otherwise would be. That principle still holds today, in some form, across most common law jurisdictions.

In practice, tax avoidance covers an enormous range of entirely legitimate activities. Maximising pension contributions in the UK to reduce your taxable income. Using a Section 1031 exchange in the US to defer capital gains on real estate. Structuring a business across EU member states to take advantage of participation exemptions on dividends. Establishing a holding company in Mauritius to access treaty benefits when investing into sub-Saharan Africa.

None of these are clever tricks. They're the tax code functioning exactly as legislators intended.

Tax Evasion: Where the Law Ends and Criminality Begins

Tax evasion is different in kind, not just degree. It involves deliberately concealing information from tax authorities — hiding income, falsifying records, failing to declare offshore accounts, or misrepresenting the nature of a transaction. The intent to deceive is the defining element. And no jurisdiction on earth — not Switzerland, not Singapore, not any African low-tax jurisdiction — provides a safe harbour for it.

The consequences are serious. In the US, federal tax evasion carries up to five years in prison and fines up to $250,000 per count. In the UK, HMRC's Fraud Investigation Service pursues criminal prosecutions with increasing vigour and can pursue assets internationally. Across the EU, the 2018 Anti-Tax Avoidance Directive (ATAD) has tightened cooperation between member states considerably. And African tax authorities — often underestimated — have been significantly empowered through the African Tax Administration Forum (ATAF) and bilateral exchange-of-information agreements.

I've seen this go wrong in ways that seemed entirely avoidable. A high-net-worth client — a business owner with operations in Nigeria, the UAE, and the UK — had structured his affairs through a series of shell companies in ways his original advisors described as "aggressive planning." What they'd actually created was a trail of undisclosed beneficial ownership that, once Nigeria's Federal Inland Revenue Service began exchanging data under the Common Reporting Standard, became extraordinarily difficult to explain. The penalties were severe. The reputational damage worse.

The Grey Zone: Aggressive Tax Avoidance That Courts Now Reject

Here's where it gets genuinely complicated. Between clearly legitimate tax planning and outright evasion sits a contested middle ground: arrangements that are technically legal but that tax authorities increasingly challenge as "artificial" or lacking commercial substance.

The OECD's Base Erosion and Profit Shifting (BEPS) project, now adopted in some form by over 140 countries, specifically targets structures where transactions are engineered for tax purposes without genuine economic activity to support them. The UK's General Anti-Abuse Rule (GAAR), the US's economic substance doctrine, and similar provisions across the EU all give tax authorities the power to recharacterise or disregard arrangements they deem abusive — even if those arrangements were technically compliant when entered into.

In my experience, the most dangerous position a taxpayer can be in isn't evasion — it's relying on aggressive avoidance schemes that were sold as bulletproof but are now squarely in regulators' crosshairs. The UK's loan charge legislation, which retrospectively taxed contractor loan schemes many people had been told were legitimate, destroyed finances that people had spent decades building. The legality had been arguable. The outcome was not.

Mini Case Study — Cross-Border Tax Planning

A South African entrepreneur with manufacturing operations in Kenya and a UK holding company came to me wanting to extract profits efficiently. Her previous structure routed dividends through a Mauritius entity — a common approach — but it had been set up without genuine substance: no local staff, no real management, just a brass-plate office.

Post-BEPS, that structure was a liability. Kenya's revised tax treaties specifically include Principal Purpose Tests that would have denied treaty benefits if challenged. We rebuilt the structure with genuine operational presence in Mauritius, ensured board meetings were held locally with qualified directors, and documented the commercial rationale thoroughly. Same tax outcome. Defensible. Sustainable. That's what good international tax strategy looks like.

Staying Compliant Across Jurisdictions: What Serious Tax Compliance Looks Like

For individuals managing cross-border wealth, the compliance landscape has changed fundamentally since 2014. The Common Reporting Standard (CRS), FATCA in the US, and beneficial ownership registers across the EU have effectively ended banking secrecy as a planning tool. Tax authorities now receive automatic information about your offshore accounts, income, and assets. Assume they know more than you think they do.

What does robust tax compliance actually require for internationally mobile, high-net-worth individuals?

- Accurate and timely filing in every jurisdiction where you have a taxable presence — this includes consideration of deemed domicile rules in the UK, worldwide income reporting requirements in the US, and controlled foreign corporation rules wherever you hold offshore entities.

- Clear documentation of commercial rationale for any structure — not just the tax rationale. Regulators want to see that your Cayman holding company or Dubai DIFC entity exists for real business reasons, not solely to reduce your tax bill.

- Proactive disclosure where past arrangements may be questionable. Voluntary disclosure programmes exist in the US (IRS Streamlined Procedures), the UK, and many African jurisdictions — the penalties are almost always materially lower than those for arrangements that are later discovered.

And here's my genuine professional opinion: the clients who sleep well at night aren't the ones with the most aggressive structures. They're the ones whose affairs can withstand full scrutiny without any document shredding required. That's not timidity — it's intelligent risk management.

What This Means for Your International Tax Strategy

The goal of sound international tax planning has never been to pay zero tax. It's to pay the right amount of tax — no more, no less — in the right jurisdictions, under the right structures, and with the right documentation. There's a meaningful difference between that and evasion, and there's also a meaningful difference between that and unnecessarily handing money to the revenue.

But the rules change. Treaties are renegotiated. BEPS continues to evolve. New reporting requirements emerge. What was a perfectly solid structure in 2015 may carry real risk today. So if your current cross-border tax arrangements haven't been reviewed since the BEPS Action Plans were implemented, or since CRS went live in your jurisdiction, that review is overdue.

The line between tax avoidance and tax evasion is clear in principle. In practice, in complex multi-jurisdictional structures, it takes expertise to stay clearly on the right side of it — and to build strategies that will still be defensible five years from now, not just today.

Ready to review your international tax structure? If you have cross-border wealth, offshore entities, or complex arrangements that haven't been properly reviewed recently, get in touch for a confidential consultation.

This article is for informational purposes only and does not constitute legal or tax advice. Consult a qualified tax professional for advice specific to your situation.